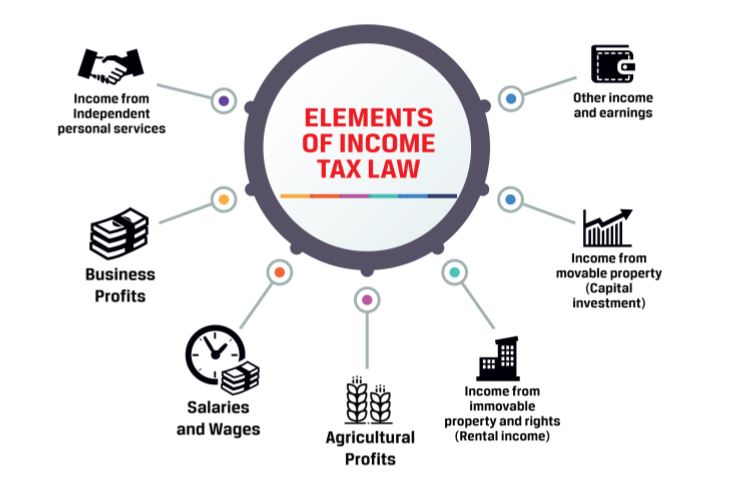

Personal income tax (PIT) is levied on the income of individuals. The term “individuals” refers to the real persons. In the application of income tax, partnerships are not deemed to be separate entities and each partner is taxed individually on his/her share of proit. An individual’s income may consist of one or more income elements listed as follows:

2. TAX LIABILITY

In general, residency criterion is applicable for determining tax liability for individuals. This criterion requires that an individual whose domicile is in Turkey is liable to pay tax for his worldwide income (unlimited liability). Any person who resides in Turkey for more than six months in a single calendar year is assumed to be a resident of Turkey. However; foreigners who stay in Turkey for six months or more by the reason of a speciic job or business or particular purposes speciied in the PIT Law are not treated as residents. Therefore, unlimited tax liability is not applicable for them.

In addition to the residency criterion, within a limited scope, nationality criterion also applies regardless of their residency status, Turkish citizens who live abroad and work for the government or a governmental institution or a company whose headquarter is in Turkey, are considered as unlimited liable taxpayers. Accordingly, they are subjected to PIT over their worldwide income. Non-residents are only liable to pay tax over their income derived from the incomes in Turkey (limited liability). For tax purposes, it is especially important to determine in what circumstances income is deemed to be derived in Turkey. The provisions of Article 7 of the PIT Law regulate this issue.

The income is assumed to be derived in Turkey in the following circumstances.

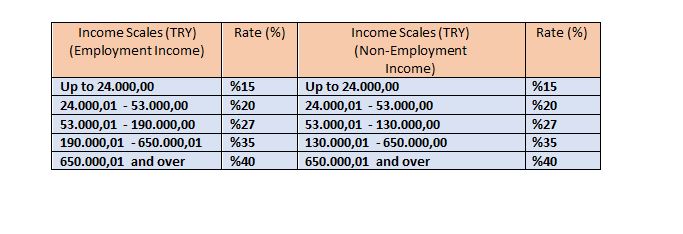

3. INCOME TAX RATES

Individual income tax rates applicable for 2019 are as follows: